Join our community of SUBSCRIBERS and be part of the conversation.

To subscribe, simply enter your email address on our website or click the subscribe button below. Don't worry, we respect your privacy and won't spam your inbox. Your information is safe with us.

The Foreign Exchange Management Act (FEMA), 1999 is a critical legislation that governs foreign exchange transactions in India. It was enacted to facilitate external trade and payments while promoting the orderly development and maintenance of the foreign exchange market in the country. Compliance with FEMA regulations is essential for individuals and organizations engaged in international financial transactions. This guide aims to provide students with a fundamental understanding of FEMA compliance.

Key Objectives of FEMA

FEMA was introduced to replace the Foreign Exchange Regulation Act (FERA), bringing a more liberalized approach to foreign exchange transactions. The primary objectives of FEMA are:

Regulating foreign exchange transactions.

Facilitating external trade and payments.

Promoting the orderly development of the foreign exchange market in India.

Maintaining foreign exchange reserves.

Key Provisions Under FEMA

FEMA classifies transactions into two broad categories:

Current Account Transactions – Payments related to trade, services, remittances, and other short-term financial dealings.

Capital Account Transactions – Investments, loans, and borrowings that affect assets and liabilities beyond India.

Basic Compliances under FEMA for Businesses

Business organizations dealing in foreign exchange must adhere to several FEMA compliances, including:

1. Know Your Customer (KYC) Norms

2. Reporting of Foreign Exchange Transactions

3. Annual Return on Foreign Liabilities and Assets (FLA Return)

8. Anti-Money Laundering (AML) and Prevention of Money Laundering Act (PMLA) Compliance

1. Know Your Customer (KYC) Norms

Businesses involved in foreign exchange transactions must comply with KYC norms to ensure transparency and prevent money laundering.

2. Reporting of Foreign Exchange Transactions

Companies must report all foreign investments, including Foreign Direct Investment (FDI), External Commercial Borrowings (ECB), and Foreign Portfolio Investment (FPI) to the Reserve Bank of India (RBI) within prescribed timelines.

3. Annual Return on Foreign Liabilities and Assets (FLA Return)

Companies receiving foreign investment must file an annual FLA return with the RBI by July 15 each year, reporting their foreign liabilities and assets.

4. Foreign Direct Investment (FDI) Compliance

Businesses must comply with sectoral FDI limits and approval routes (automatic or government approval).

Companies must file Form FC-GPR with the RBI within 30 days of issuing shares to foreign investors.

Transfers of shares to or from foreign entities must be reported using Form FC-TRS.

Businesses obtaining foreign loans must report ECB transactions via Form ECB 2 Return to the RBI monthly.

ECB funds must be used for permitted purposes as per sector-specific guidelines.

6. Overseas Direct Investment (ODI) Compliance

Indian businesses investing abroad must file Form ODI with the RBI.

They must report financial commitments and transactions related to foreign subsidiaries or joint ventures.

Regular disclosures on financial performance and repatriation of investments are mandatory.

7. Liberalized Remittance Scheme (LRS) Compliance

Businesses making permissible remittances under LRS must ensure proper reporting.

Transactions must comply with RBI guidelines and sectoral restrictions.

8. Anti-Money Laundering (AML) and Prevention of Money Laundering Act (PMLA) Compliance

Businesses must establish policies to monitor and report suspicious foreign exchange transactions.

Compliance with Financial Intelligence Unit (FIU-IND) reporting requirements is essential.

Penalties for Non-Compliance

Failure to comply with FEMA regulations can lead to severe penalties, including:

A fine of up to three times the amount involved in the contravention

Confiscation of assets or properties involved in the violation

Legal action and enforcement proceedings by the Directorate of Enforcement

Conclusion

For business organizations engaged in cross-border trade and financial transactions, FEMA compliance is a legal necessity. Proper adherence to FEMA regulations helps maintain financial stability, fosters international trade, and avoids regulatory complications. Companies should ensure periodic reviews and compliance audits to remain aligned with FEMA guidelines and avoid penalties.

Buyer’s credit refers to a loan or credit facility provided to the buyer (importer) to finance the purchase of goods or services from a foreign seller (exporter). It is often facilitated by a bank or financial institution and is commonly used in international trade when the buyer needs additional funds to complete the transaction. Unlike other forms of credit, buyer’s credit focuses on providing financing for buyers to pay the seller directly, ensuring that the transaction is completed smoothly.

Features of Buyer’s Credit:

Loan to the Buyer: The bank or financial institution provides the buyer with a loan to pay the seller. The buyer repays the loan with interest over a predetermined period.

Typically Long-Term: Buyer’s credit often comes with longer repayment terms, such as 3 to 5 years, depending on the size and nature of the transaction.

Used for Large Transactions: This form of credit is commonly used in industries like construction, infrastructure, and large-scale machinery procurement, where the buyer may not have sufficient immediate funds but can afford longer repayment terms.

International Trade: It is mostly used in cross-border transactions where buyers need financing to complete payments for imported goods and services.

Advantages of Buyer’s Credit:

Flexible Financing: It allows buyers to procure goods or services without having to use their own capital upfront.

Cost Efficiency: By securing financing through buyer’s credit, the buyer may get better interest rates compared to other loan types, especially if the credit is backed by a reputable financial institution.

Promotes Trade: Buyer’s credit helps exporters increase sales by providing buyers with the financial flexibility they need

Buyer's Credit can be issued without a Letter of Credit (LC), but it is less common. Typically, Buyer's Credit is linked to an LC because LCs provide security for both the buyer and the lender.

A Letter of Credit (LC) is a financial document issued by a bank on behalf of a buyer, guaranteeing payment to the seller, provided that the terms and conditions stipulated in the LC are met. LCs are commonly used in international trade to reduce the risk of non-payment and ensure that the seller is compensated for goods or services once the required documentation is provided.

Various types of LCs:

· Revocable Letter of Credit:Can be modified or canceled by the buyer (or applicant) or the issuing bank at any time before payment is made. Offers less security to the seller as the terms are not fixed.

· Irrevocable Letter of Credit: Cannot be changed or canceled without the consent of all parties involved (the buyer, seller, and bank). Provides more security for the seller compared to a revocable LC.

· Confirmed Letter of Credit :Involves a second bank (usually the seller’s bank) confirming the LC. The confirming bank guarantees payment, even if the issuing bank defaults. It adds an extra layer of security for the seller.

· Unconfirmed Letter of Credit: A Letter of Credit where only the issuing bank is responsible for payment, without any confirmation from another bank. Offers less security for the seller.

· Sight Letter of Credit: Payment is made immediately when the required documents are presented to the bank and verified. Commonly used in cases where the buyer and seller have a high level of trust.

· Time or Usance Letter of Credit: Payment is made after a specified period, typically 30, 60, or 90 days from the date of shipment or presentation of documents. Used when the buyer requires time to make the payment.

· Standby Letter of Credit: Acts as a guarantee of payment in case the buyer defaults on their contractual obligations. It is often used as a backup payment method.

Benefits of Using a Letter of Credit

Security for Sellers: Provides assurance of payment once the terms are met, reducing the risk of non-payment.

Risk Mitigation for Buyers: Buyers can ensure that payment is only made when the seller fulfills their obligations, such as shipping the goods.

Facilitates International Trade: Helps establish trust between parties who may not know each other, especially in cross-border transactions.

Key Features of a Letter of Credit

1.Parties Involved:

Applicant: The buyer (importer) who requests the LC from their bank.

Beneficiary: The seller (exporter) who receives the payment.

Issuing Bank: The bank that issues the LC on behalf of the buyer.

Advising Bank: The bank that advises the beneficiary about the LC, usually located in the beneficiary’s country.

2. Documents Required: To receive payment, the beneficiary must present specific documents, which may include:

Bill of lading

Commercial invoice

Insurance certificate

Packing list

Any additional documents specified in the LC.

3. Payment Guarantee: The LC guarantees that as long as the beneficiary presents the required documents that comply with the terms of the LC, the issuing bank will make the payment.

4. Conditions and Terms: The LC will specify the conditions under which the payment will be made, including the timeframe for document submission and any specific requirements related to the shipment of goods.

LCs are bank-backed guarantees that secure international trade. They mitigate risk for both buyers and sellers by ensuring payment upon fulfillment of agreed-upon conditions, fostering trust and facilitating cross-border transactions.

Bank credit refers to the amount of money or financial resources a bank extends to its customers, which can be in the form of loans, overdrafts, or credit facilities. Bank credits enable businesses to manage cash flow, finance operations, and support short-term or long-term growth.

Types of Bank Credit:

1. Term Loan

2. Demand Loan

3. Overdraft

1.TERM LOAN

A Term Loan is a type of loan that is borrowed for a specific amount and must be repaid in regular installments over a fixed period. It is commonly used for funding business expansion, purchasing equipment, or personal purposes like home or car loans.

Key Features of Term Loans:

Fixed Repayment Period – The loan is repaid over a predetermined period (short-term, medium-term, or long-term).

Regular Installments – Repayment is done in Equated Monthly Installments (EMIs).

Secured or Unsecured – Can be backed by collateral (e.g., property, machinery) or be unsecured based on creditworthiness.

Fixed or Floating Interest Rate – The interest can be either fixed throughout the tenure or variable.

2. DEMAND LOAN:

A Demand Loan is a type of loan that a lender (eg Bank) can demand full repayment of at any time. Under demand loan borrower must repay the loan immediately when the lender requests it.

Key Features of Demand Loans:

No Fixed Repayment Period – The lender can recall the loan at any time.

Short-Term in Nature – Typically used for short-term financial needs.

Secured or Unsecured – Can be backed by collateral or granted based on creditworthiness.

3.OVERDRAFT FACILITY

An Overdraft Facility is a financial arrangement where a bank allows a customer to withdraw more money than what is available in their account. It is like a short-term loan and is typically linked to a current account

Key Features of Overdraft Facility:

Pre-Approved Limit – Banks set a maximum overdraft limit based on creditworthiness.

Interest on Used Amount – Interest is charged only on the amount utilized, not on the entire limit.

Flexible Repayment – Borrowers can repay anytime within the overdraft tenure.

Secured or Unsecured – Can be backed by collateral (e.g., fixed deposits) or offered without security.

Bank credits help businesses smooth their financial operations, ensuring liquidity even when cash flow is inconsistent. However, obtaining bank credit requires a solid business plan, good credit history, and sometimes collateral.

The Union Budget 2025 introduced several significant amendments to the Tax Deducted at Source (TDS) provisions, aiming to simplify tax compliance and enhance financial flexibility for taxpayers. Key changes include:

1. Section 194 :– TDS on Dividend:– Limit substituted from Rs. 5,000/- to Rs. 10,000/-

2. Section 194A:-TDS on Interest other than securities: – Limit substituted as:

Taxpayer bank/Co- operative society and Post office

Taxpayer other than Bank/Co- operative Society and Post Office:

For General: – limit substituted from 40,000/- to 50,000/- Rs

Limit substituted from 5,000/- Rs to Rs. 10,000/-

For Senior Citizen: – limit substituted from Rs. 50000/- to 1,00,000/- lac

3. Section 194B:-any person who pays any sum in the form of winnings from any lottery or crossword puzzle or card games or other games of any sort : instead of aggregate threshold limit exceeding during the financial year removed and in respect of single transaction is substituted.

4. Section 194D:-Tax Deducted at Source (TDS) on payments made under life insurance policies any payment or reward in the form of commission exceeding Rs 15000/- substituted to Rs 20000/-

5. Section 194G:- TDS on Commission on Sale of Lottery Tickets The Deductor would be liable to deduct TDS under section 194G only if the income amount exceeds Rs.15,000. The limit substituted from Rs.15,000/- to Rs 20,000/-

6. Section 194H:- TDS on Commission The Deductor would be liable to deduct TDS under section 194H only if the income amount exceeds INR 15,000. The limit substituted from Rs. 15000/- to Rs 20000/-

7. Section 194I:- TDS on Rent “Provided that no deduction shall be made under this section, where the income by way of rent credited or paid for a month or part of a month by such person to the account of, or to, the payee, does not exceed fifty thousand rupees:”. i.e. Rs. 6,00,000/- in a year.

8. Section 194J:- TDS on Profession “The Deductor would be liable to deduct TDS under section 194J only if the amount paid exceeds INR 30,000. The limit substituted from Rs. 30,000/- to Rs 50,000/-

9. Section 194K:- Taxation income on dividend from mutual fund “The Deductor would be liable to deduct TDS under section 194k only if the amount paid exceeds Rs.5,000. The limit substituted from Rs.5,000/- to Rs 10,000/-

10. Section 194L:- payment of compensation on acquisition of capital asset “The Deductor would be liable to deduct TDS under section 194l only if the amount paid exceeds Rs. 2,50,000. The limit substituted from Rs.2,50,000/- to Rs 5,00,000/-

11. Section 194LBC:- income distributed by a specified entity to its unit holders Section 194LBC of the Act requires that where any income is payable by a securitization trust to an investor, being a resident, in respect of an investment in a securitization trust as specified therein, the person responsible for making the payment shall, deduct income-tax, at the rate of 10%, if the payee is an individual or a Hindu undivided family and 10%, if the payee is any other person.

12. Section 194Q:- is a provision for Tax Deducted at Source (TDS) applicable to specific high-value goods purchases only TDS under Section 194Q will now apply to the purchase of goods exceeding Rs. 50 lakh.

Section 206C(1H) was omitted, which previously required the collection of tax at source (TCS) on the sale of goods exceeding Rs. 50 lakh.

13. Section 194S: TDS on transfer of Virtual Digital Assets (VDA) section 206AB higher rate of TDS if no PAN furnished removed.

14. Section 206AB: omitted Deduct TDS at higher rates than usual when you make payments to those who have not filed their income tax return in the last year now excludes from income tax

Salicornia brachiata is a halophyte, meaning it is a salt-tolerant plant that typically grows/found in saline environments such as coastal areas, salt marshes, and tidal flats. It belongs to the family Amaranthaceae and is part of the genus Salicornia, which is commonly known as Glasswort, Samphire, Sea Asparagus, Pickleweed, Umari and Keerai.

Key Features of Salicornia brachiata:

Habitat: It thrives in salty or brackish environments and is well-adapted to withstand high salinity levels.

Appearance: The plant is succulent and fleshy, with segmented, cylindrical stems that are often green but may turn reddish under stress or during certain seasons.

Uses:

Culinary: Some Salicornia species are edible and used as a vegetable or garnish in coastal cuisines. However, the specific culinary use of S. brachiata depends on local practices.

Ecological: It plays a role in stabilizing coastal ecosystems, preventing soil erosion, and improving saline soil quality.

Biotechnological: This plant has gained attention for its potential in bio-saline agriculture, phytoremediation, and as a source of bioactive compounds. It is particularly noted for its antioxidant and medicinal properties.

Economic Importance:

Salicornia brachiata is being researched as a source of biodiesel due to its ability to produce oils under saline conditions.

It may also be used for the extraction of bioactive compounds like flavonoids and phenolics.

Conservation and Challenges

Although it is resilient, Salicornia brachiata may face threats from habitat loss, pollution, and climate change, which can affect coastal and saline ecosystems where it grows.

A Data Migration Audit is the process of reviewing and validating the migration of data from one system, database, or format to another. It ensures that data has been transferred accurately, completely, and securely, without loss, corruption, or unauthorized access. This audit is a critical component of any data migration project, as it helps to identify discrepancies and ensures compliance with regulatory and business requirements.

Why is it Important?

Data Accuracy: Ensures the integrity and accuracy of data in the target system.

Compliance: Verifies adherence to regulatory standards.

Risk Mitigation: Identifies and addresses issues before they impact business processes.

Business Continuity: Ensures migrated data supports seamless operation.

What are some types of data migration?

Database migration: Moving a database to a new device or cloud

Application migration: Moving an application from one server or storage location to another

Cloud migration: Moving data or applications from an on-premises location to the cloud

Business process migration: Moving business applications and processes to a new environment

How to Perform a Data Migration Audit

The audit typically follows these steps:

Pre-Migration Planning

Data Mapping and Transformation Validation.

Test Migration

Post-Migration Validation

Audit Logs and Monitoring

Stakeholder Review

Documentation and Reporting

Ongoing Monitoring

1. Pre-Migration Planning

Define Objectives: Determine the purpose and scope of the migration.

Create an Audit Plan: Include specific checks, milestones, and reporting requirements.

Inventory Existing Data: Understand the structure, quality, and volume of the data to be migrated.

Establish Metrics: Define success criteria for accuracy, completeness, and performance.

2. Data Mapping and Transformation Validation

Map Source to Target: Verify that all data fields are correctly mapped to the target system.

Transformation Rules: Check that data transformations (e.g., format changes, conversions) are accurate and consistent.

3. Test Migration

Run a Pilot Test: Migrate a subset of data to validate the process.

Reconcile Source and Target Data: Compare data in the source and target systems to identify mismatches.

Verify Dependencies: Ensure related records and dependencies are maintained.

4. Post-Migration Validation

Data Completeness Check: Confirm that all records were migrated without loss.

Accuracy Check: Verify data consistency between source and target.

Business Process Testing: Ensure migrated data supports critical business functions.

5. Audit Logs and Monitoring

Review Logs: Examine system logs to detect errors or anomalies during migration.

Track Changes: Ensure changes to data during migration are documented and authorized.

6. Stakeholder Review

User Acceptance Testing (UAT): Involve business users to validate data usability in the target system.

Sign-Off: Obtain formal sign-off from stakeholders before decommissioning the source system.

7. Documentation and Reporting

Audit Report: Document findings, including errors, resolutions, and final validations.

Compliance Records: Retain evidence of the audit for regulatory purposes.

8. Ongoing Monitoring

Post-Migration Monitoring: Implement mechanisms to monitor data quality and performance over time.

Lessons Learned: Use insights from the audit to improve future migrations.

Tools and Technologies for Data Migration Audits

Data Profiling and Quality Tools: Help to identify data quality issues and assess data completeness.

Data Comparison Tools: Facilitate the comparison of source and target data to identify discrepancies.

Data Visualization Tools: Help to visualize data and identify patterns and trends.

Automation Tools: Automate repetitive audit tasks, such as data collection and analysis.

व्यवसाय और व्यापार आर्थिक गतिविधियों के दो हिस्से हैं, लेकिन इनके उद्देश्य, कार्यप्रणाली और दायरे में कई स्पष्ट अंतर हैं। दोनों का योगदान अर्थव्यवस्था में विशेष है, लेकिन इनका स्वरूप भिन्न है।

1. व्यवसाय व व्यापार की परिभाषा

व्यवसाय:

व्यवसाय एक व्यापक गतिविधि है, जिसमें किसी उत्पाद या सेवा का उत्पादन, वितरण और विपणन शामिल है। इसका उद्देश्य मानव की आहार,आवास, अलंकार व दूर गमन, दूर श्रवण तथा दूर दर्शन आदि आवश्यकताओं को पूरा करना है l व्यवसाय मानव में समृद्धि भावना का अवसर प्रदान करता है ।

व्यापार:

व्यापार मुख्य रूप से वस्तुओं और सेवाओं की खरीद-बिक्री से जुड़ा होता है। इसका उद्देश्य तैयार माल का लेन-देन करके मुनाफा कमाना मात्र होता है। यहाँ पर यह भी देखा जाता है ब्यापार करने बाला मानव कम देकर अधिक लेने की भावना से ग्रसित रहता हैI

2. व्यवसाय व व्यापार के उद्देश्य

व्यवसाय:

उत्पादों और सेवाओं का निर्माण व उपभोक्ताओं तक पहुंचाना।

मानव जाति की आवश्यकताओं को पूरा करना।

आर्थिक और सामाजिक मूल्य सृजित करना।

व्यापार:

तैयार वस्तुओं को खरीदना और बेचना।

तुरंत लाभ अर्जित करना।

कम देकर अधिक लेन पर केंद्रित रहना।

3. व्यवसाय व व्यापार के स्वरूप

व्यवसाय:

विस्तृत गतिविधि।

उत्पादन, वित्त, विपणन और मानव संसाधन जैसे कई घटक।

व्यापक व सामाजिक स्तर पर संचालन।

व्यापार:

सरल गतिविधि।

केवल खरीद और बिक्री तक सीमित।

सीमित भूमिका।

4. उद्यम के प्रकार

व्यवसाय:

उद्योग: उत्पादन, निर्माण, और कारखाने से जुड़े कार्य।

शिक्षा विनिमय-कोष, स्वास्थ-सयम सेवा क्षेत्र: बैंकिंग, स्वास्थ्य सेवाएं, शिक्षा।

व्यापार को व्यवसाय से अलग होकर अपना कोई अस्तित्व नहीं हैl

व्यापार:

आंतरिक व्यापार: देश के भीतर वस्तुओं और सेवाओं का आदान-प्रदान।

बाहरी व्यापार: आयात और निर्यात।

निष्कर्ष व्यवसाय और व्यापार में सबसे बड़ा अंतर इनके दायरे और स्वरूप में है। व्यवसाय, व्यापक और बहुआयामी है, जो उत्पादन से लेकर विपणन तक के सभी पहलुओं को समेटता है। व्यापार मात्र वस्तुओं और सेवाओं के लेन-देन पर केंद्रित है। व्यवसाय का लक्ष्य मानव समृद्धि निर्माण है, जबकि व्यापार का उद्देश्य तात्कालिक मुनाफा अर्जित करना हैl

ये लेखक के अपने विचार हैं हो सकता है आप सहमत न हों

Banking services encompass a wide range of financial products and services provided by banks to individuals, businesses, and institutions. Here’s an overview of the key types of banking services:

Depositor

Financial Intermediaries

Borrowers

● Payment services

● Deposit and Lending services

● Investment, pensions, and insurance

● E-banking

PAYMENT SERVICES

Payment services encompass a range of methods and systems that enable individuals and businesses to transfer funds and settle transactions. These services are essential for facilitating commerce, both online and offline. Here’s an overview:

Types of Payment Services

Traditional Payment Methods:

Cash: Physical currency used for in-person transactions.

Checks: Written orders directing a bank to pay a specific amount from the account of the writer.

Electronic Payment Methods:

Debit Cards: Linked directly to a bank account, allowing users to spend only what they have.

Credit Cards: Allow users to borrow funds up to a limit, to be paid back later with interest.

Prepaid Cards: Loaded with a specific amount of money in advance for spending.

Online Payment Services:

Payment Gateways: Facilitate online transactions between customers and merchants (e.g., PayPal, Stripe).

E-wallets: Digital wallets that store payment information and allow for easy online purchases (e.g., Google Pay, Apple Pay).

Mobile Payment Solutions:

Mobile Banking Apps: Allow users to manage bank accounts and make payments through their smartphones.

Contactless Payments: Enable transactions through NFC technology using smartphones or contactless cards.

Automated Clearing House (ACH):

A network for electronically transferring funds between banks, commonly used for direct deposits and bill payments.

DEPOSIT SERVICES AND LENDING SERVICES

Deposit and lending services are core functions of banks and financial institutions. Deposit and lending services are fundamental to the functioning of the banking system and play a crucial role in personal and business finance. Understanding these services helps individuals and businesses make informed financial decisions.

DEPOSIT SERVICES

Deposit services allow customers to place their money in a bank or financial institution for safekeeping, earning interest in the process. Key types include:

Savings Accounts:

Definition: Accounts designed to hold funds while earning interest.

Features: Typically offer lower interest rates, with limited withdrawal options.

Current Accounts:

Definition: Transaction accounts primarily for businesses or frequent transactions.

Features: Usually no interest, with unlimited deposits and withdrawals, often accompanied by check-writing privileges.

Fixed Deposits (FDs):

Definition: Accounts where money is deposited for a fixed term at a higher interest rate.

Features: Early withdrawal may incur penalties; interest rates are typically higher than savings accounts.

Recurring Deposits (RDs):

Definition: Accounts that allow customers to deposit a fixed amount regularly.

Features: Ideal for saving over time, offering a fixed interest rate.

Money Market Accounts:

Definition: Hybrid accounts that combine features of savings and checking accounts.

Features: Typically offer higher interest rates with limited check-writing abilities.

LENDING SERVICES AND BANK CREDIT

Lending services enable banks to provide loans to individuals and businesses, allowing them to borrow funds for various purposes.

Personal Loans:

Definition: Unsecured loans for personal use, such as medical expenses or vacations.

Features: Fixed interest rates and monthly payments; often based on creditworthiness.

Home Loans (Mortgages):

Definition: Loans specifically for purchasing real estate.

Features: Typically secured by the property, with long repayment terms (15-30 years).

Business Loans:

Definition: Loans aimed at financing business operations or expansion.

Features: Can be secured or unsecured, with varying terms based on the business’s financial health.

Auto Loans:

Definition: Loans for purchasing vehicles.

Features: Usually secured by the vehicle itself, with fixed repayment terms.

Student Loans:

Definition: Loans to cover educational expenses.

Features: Often have deferred repayment options until after graduation.

Payday Loans:

Definition: Short-term, high-interest loans meant to cover immediate expenses until the next paycheck.

Features: High fees and interest rates; typically should be avoided unless absolutely necessary.

Bank credit refers to the loans and advances provided by a bank to individuals or companies. These include different types of credit facilities such as:

•Term Loans: These are loans provided for a specific time period and are usually for large capital expenditures.

•Cash Credit: A short-term loan provided to businesses to meet working capital needs. It is usually secured by the company’s inventory or receivables.

•Overdraft: This allows a borrower to withdraw more than what is available in their account, up to a predetermined limit.

•Trade Credit: A credit extended by banks for trade-related purposes, such as import-export financing.

INVESTMENT, PENSIONS, AND INSURANCE SERVICES

Investment, pensions, and insurance services are essential components of financial planning, providing individuals and businesses with tools to manage risks, save for the future, and grow wealth. Here’s an overview of each:

Investment Services

Investment services help individuals and institutions allocate their funds to various assets with the aim of growing wealth over time. Key components include:

Stocks:

Definition: Shares of ownership in a company.

Features: Potential for capital appreciation and dividends; higher risk compared to other investments.

Bonds:

Definition: Debt securities issued by corporations or governments.

Features: Generally considered safer than stocks, providing fixed interest payments and principal repayment at maturity.

Mutual Funds:

Definition: Investment vehicles that pool money from multiple investors to buy a diversified portfolio of stocks, bonds, or other securities.

Features: Managed by professional fund managers; offers diversification and liquidity.

Exchange-Traded Funds (ETFs):

Definition: Similar to mutual funds but traded on stock exchanges like individual stocks.

Features: Typically lower fees and provide flexibility for buying and selling throughout the day.

Real Estate:

Definition: Physical properties purchased for rental income or capital appreciation.

Features: Provides potential for cash flow and tax benefits but involves more management and less liquidity.

Alternative Investments:

Definition: Investments outside of traditional asset classes, such as hedge funds, commodities, and collectibles.

Features: Often used for diversification; may have higher risks and lower liquidity.

Pension Services

Pension services provide retirement income to individuals, helping them save for their post-work life. Key types include:

Defined Benefit Plans:

Definition: Employer-sponsored plans that promise a specific payout upon retirement, based on salary and years of service.

Features: Provides predictable income but relies on employer funding and management.

Defined Contribution Plans:

Definition: Retirement plans where employees and/or employers contribute a set amount, with payouts based on investment performance (e.g., 401(k) plans).

Features: More common today; benefits depend on investment choices and market performance.

Individual Retirement Accounts (IRAs):

Definition: Personal retirement savings accounts with tax advantages.

Types: Traditional IRAs (tax-deferred contributions) and Roth IRAs (tax-free withdrawals).

Annuities:

Definition: Insurance products that provide regular income payments in exchange for a lump sum payment or series of payments.

Features: Can be fixed or variable; used for retirement income stability.

Insurance Services

Insurance services protect individuals and businesses from financial losses due to unforeseen events. Key types include:

Life Insurance:

Definition: Provides a payout to beneficiaries upon the insured’s death.

Types: Term life (coverage for a specific period) and whole life (permanent coverage with a cash value component).

Health Insurance:

Definition: Covers medical expenses for illnesses, injuries, and other health-related costs.

Types: Employer-sponsored plans, government programs (e.g., Medicare), and individual plans.

Property and Casualty Insurance:

Definition: Protects against loss or damage to property and liability for accidents (e.g., homeowners and auto insurance).

Features: Covers damages, theft, and liability claims.

Disability Insurance:

Definition: Provides income replacement if the insured becomes unable to work due to a disability.

Features: Short-term and long-term policies are available.

Liability Insurance:

Definition: Protects against claims resulting from injuries or damage to other people or property.

Types: General liability, professional liability (errors and omissions), and product liability.

E-BANKING

E-banking, or electronic banking, refers to the use of digital platforms and technology to manage banking services and conduct financial transactions. It provides customers with a convenient way to access banking services from anywhere, at any time.

Key Features of E-Banking

Online Account Management:

Customers can view account balances, transaction history, and statements.

Users can manage multiple accounts (checking, savings, and loans) from a single interface.

Fund Transfers:

Internal Transfers: Move money between accounts within the same bank.

External Transfers: Send money to accounts at other banks, often through services like NEFT, RTGS, or IMPS.

Bill Payments:

Users can pay utility bills, credit card bills, and other payments electronically.

Scheduled payments can be set up for convenience.

Mobile Banking:

Banking apps allow access to services via smartphones or tablets.

Features include mobile deposits, location-based services, and notifications.

Online Loan Applications:

Customers can apply for personal, home, or auto loans online.

Pre-approval and instant loan status updates are often available.

Investment Services:

Access to investment accounts for stocks, mutual funds, and retirement accounts.

Online trading platforms may also be available.

Customer Support:

E-banking platforms typically offer live chat, email support, or FAQs for assistance.

Automated catboats can provide 24/7 support for common queries.

Benefits of E-Banking

Convenience: Access banking services 24/7 from anywhere with an internet connection.

Time-Saving: Quick transactions without the need to visit a physical bank branch.

Cost-Effective: Often lower fees for online transactions and services.

Enhanced Security: Banks implement various security measures, such as encryption and two-factor authentication, to protect users’ data.

Security Measures

Encryption: Sensitive data is encoded to prevent unauthorized access during transmission.

Two-Factor Authentication (2FA): Requires users to verify their identity through a second method (e.g., SMS code, authenticator app).

Secure Socket Layer (SSL): Ensures secure connections between users and the bank’s website.

Fraud Detection: Banks employ systems to monitor and flag suspicious transactions.

Challenges of E-Banking

Cyber security Risks: Threats such as phishing, malware, and hacking can compromise account security.

Technical Issues: System outages or technical glitches may temporarily disrupt access to services.

Digital Divide: Not all individuals have equal access to technology or the internet, which can limit e-banking adoption.

FOREIGN EXCHANGE TRANSACTIONS AND TRADE FINANCE

Banking system provides various forms of trade finance that helps facilitate import and export business. There are three main types of trade finance:

Letters Of Credit (LC)

Standby Letter Of Credit (SBLC)

Buyer’s Credit

Foreign Bank Guarantee

LETTER OF CREDIT (LC)

A Letter of Credit (LC) is a financial document issued by a bank, guaranteeing that a buyer’s payment to a seller will be received on time and for the correct amount. LC is a vital instrument in international trade, providing security and facilitating transactions between buyers and sellers.

Process: The issuing bank ensures that payment will be made if the seller fulfills the terms agreed upon in the LC contract, such as delivering goods and services as specified

Key Features of a Letter of Credit

Parties Involved:

Applicant: The buyer (importer) who requests the LC from their bank.

Beneficiary: The seller (exporter) who receives the payment.

Issuing Bank: The bank that issues the LC on behalf of the buyer.

Advising Bank: The bank that advises the beneficiary about the LC, usually located in the beneficiary’s country.

Documents Required:

To receive payment, the beneficiary must present specific documents, which may include:

Bill of lading

Commercial invoice

Insurance certificate

Packing list

Any additional documents specified in the LC.

Payment Guarantee:

The LC guarantees that as long as the beneficiary presents the required documents that comply with the terms of the LC, the issuing bank will make the payment.

Conditions and Terms:

The LC will specify the conditions under which the payment will be made, including the timeframe for document submission and any specific requirements related to the shipment of goods.

Benefits of Using a Letter of Credit

Security for Sellers: Provides assurance of payment once the terms are met, reducing the risk of non-payment.

Risk Mitigation for Buyers: Buyers can ensure that payment is only made when the seller fulfills their obligations, such as shipping the goods.

Facilitates International Trade: Helps establish trust between parties who may not know each other, especially in cross-border transactions.

Risks and Considerations

Document Discrepancies: If the documents presented do not match the terms of the LC, payment may be delayed or denied.

Costs: There are fees associated with issuing and processing an LC, which can add to transaction costs.

Complexity: Understanding the requirements and terms of an LC can be complicated, necessitating careful attention to detail.

Types of Letters of Credit:

•Revocable vs. Irrevocable:

Revocable: Can be amended or canceled by the issuing bank without notice to the beneficiary.

Irrevocable: Cannot be changed or canceled without the consent of all parties.

Sight vs. Time:

Sight: Payment is made immediately upon presentation of the required documents.

Time: Payment is made at a later date, typically after a specified period.

•Confirmed LC: Another bank guarantees payment in addition to the issuing bank.

•Standby LC: This is a secondary payment method if the buyer fails to make payment.

STANDBY LETTER OF CREDIT (SBLC)

A Standby Letter of Credit (SBLC) is a financial instrument issued by a bank to guarantee payment to a beneficiary in the event that the applicant fails to fulfill their contractual obligations. In Standby L/C the importer’s bank makes a payment only if its customer fails to fulfill their obligations (i.e., in case of default). Therefore, the standby L/Cs issued by the importer’s bank obligates that bank to compensate the exporter only in the event of a performance failure. The importer will obviously pay a fee for this service and will be liable to its bank for any payments made by the bank under the standby L/C. Here’s an overview of SBLCs, including their features, uses, and benefits:

Key Features of Standby Letters of Credit

Guarantee of Payment:

The SBLC acts as a backup payment method, ensuring that the beneficiary receives payment if the applicant defaults on their obligations.

Conditions for Payment:

The beneficiary must present specific documents to the issuing bank that prove the applicant has failed to meet their obligations, such as invoices or contracts.

Types of SBLCs:

Performance SBLC: Guarantees the performance of contractual obligations.

Financial SBLC: Ensures payment for financial transactions, such as loans or debts.

Expiration Date:

SBLCs typically have an expiration date, after which they are no longer valid.

Transferability:

Some SBLCs can be transferred to another party, providing flexibility in transactions.

Uses of Standby Letters of Credit

International Trade:

Commonly used in international transactions where trust between parties may be low. An SBLC provides assurance to the seller.

Construction Contracts:

Used to guarantee performance and completion of projects by contractors.

Lease Agreements:

Often required in lease agreements to ensure rent payments or property maintenance.

Loan Transactions:

Banks may request an SBLC from borrowers to guarantee repayment of loans.

Benefits of Standby Letters of Credit

Risk Mitigation:

Reduces the risk for sellers and lenders by ensuring payment in case of non-performance.

Increased Credibility:

Helps businesses enhance their creditworthiness, especially for new or less established companies.

Facilitates Financing:

Allows for smoother negotiations and transactions, as parties have a security net in place.

Flexibility:

Can be tailored to meet the specific needs of the transaction and the parties involved.

Process of Obtaining a Standby Letter of Credit

Application: The applicant approaches their bank with a request for an SBLC, providing necessary documentation about the transaction.

Credit Assessment: The bank evaluates the applicant’s creditworthiness and the nature of the transaction.

Issuance: Once approved, the bank issues the SBLC, which outlines the terms and conditions.

Use in Transaction: The applicant provides the SBLC to the beneficiary as part of the contractual agreement.

Claim Process: If the applicant defaults, the beneficiary can claim payment by presenting the required documents to the issuing bank.

BUYER’S CREDIT

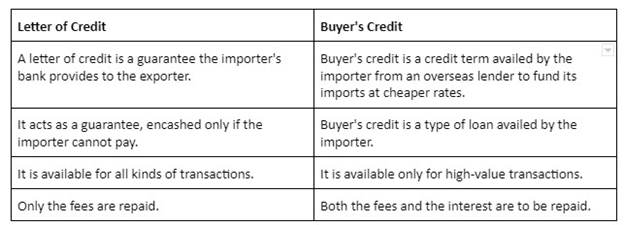

Buyers credit is a loan facility while letter of credit is a promise given by a bank to the seller that payment will be received on time. If the buyer cannot pay, the bank will be responsible for the entire amount of the purchase. Buyer’s credit is a credit facility available to importers from a foreign lender. This is usually a foreign bank or institution in the exporting country.One of the main advantages of using buyer’s credit instead of a normal LC is that the borrower wants the funding in foreign currency so that the importer can make payments to the exporter on time and in the currency of the exporter’s country.

What is the difference between letter of credit and buyer’s credit?

The fundamental difference between LC and buyer’s credit is that buyer’s credit is a loan that an importer takes and LC is a payment guarantee that an exporter uses.

It is important to note that in practice buyer’s credit may be issued on the basis of a letter of credit. This shows that structurally the two products are completely different.

FOREIGN BANK GUARANTEE

A foreign bank guarantee is a financial instrument issued by a bank in one country to provide a guarantee on behalf of a client (the applicant) to a beneficiary in another country. This instrument serves as a promise that the bank will fulfill a financial obligation if the applicant defaults on their commitments.

Key Features of Foreign Bank Guarantees

Types of Guarantees:

Performance Guarantee: Ensures the applicant completes a project or service as agreed.

Financial Guarantee: Ensures payment of a specified amount, often used in loans and credit transactions.

Advance Payment Guarantee: Protects the beneficiary if the applicant fails to refund an advance payment.

Cross-Border Transactions:

Facilitates international trade by providing assurance to foreign suppliers or service providers.

Risk Mitigation:

Reduces the risk for beneficiaries, allowing them to engage with foreign clients with greater confidence.

Documentation:

Typically requires documentation like contracts, invoices, and proof of the financial obligation.

Process of Obtaining a Foreign Bank Guarantee

Application:

The applicant approaches a bank to request a guarantee, providing relevant documentation about the transaction or contract.

Credit Assessment:

The bank evaluates the applicant’s creditworthiness and the nature of the guarantee.

Issuance:

Once approved, the bank issues the guarantee, outlining the terms and conditions, including the amount and duration.

Notification:

The bank notifies the beneficiary of the guarantee, specifying the terms under which it can be claimed.

Claim Process:

If the applicant defaults, the beneficiary can claim payment by presenting required documents to the issuing bank.

Benefits of Foreign Bank Guarantees

Enhanced Credibility:

Increases the credibility of the applicant in international transactions.

Facilitates Trade:

Encourages international trade by reducing perceived risks for foreign partners.

Flexibility:

Can be tailored to specific transactions and requirements.

Legal Protection:

Provides legal assurance to the beneficiary, as the guarantee is a formal obligation of the bank.

FEMA governs all foreign exchange transactions in India. It is essential for companies and individuals involved in foreign exchange to comply with FEMA regulations. Key compliances include:

Importers

Import Documentation: Maintain accurate documentation for all imports, including invoices, shipping documents, and customs clearance forms.

Payment for Imports: Ensure that payments for imports comply with the limits set under FEMA, and payments should typically be made in convertible foreign exchange.

Import Declaration: File an Import Declaration with the Customs Department at the time of import to ensure compliance with regulations.

Reporting Requirements: If an importer receives foreign investment, they must report this to the Reserve Bank of India (RBI) using the appropriate forms (e.g., FC-GPR).

Foreign Exchange Management: Ensure that all foreign exchange transactions related to imports are executed through authorized dealers.

Compliance with Customs Regulations: Abide by customs regulations, including the payment of applicable duties and taxes.

Advance Payment for Imports: If making advance payments, ensure compliance with guidelines regarding the maximum amount and documentation required.

Exporters

Export Documentation: Maintain proper documentation for all exports, including export invoices, packing lists, and shipping bills.

Realization of Export Proceeds: Ensure that export proceeds are realized within the specified period (usually within nine months from the date of export).

Reporting Requirements: Exporters must report their export transactions to the RBI using the specified formats (e.g., Export Declaration Form) and ensure compliance with the Foreign Exchange Management (Export of Goods and Services) Regulations.

Utilization of Export Proceeds: Ensure that the proceeds from exports are utilized in accordance with FEMA regulations, and repatriate any amounts to India within the prescribed time.

Foreign Exchange Accounts: Maintain any foreign currency accounts in compliance with RBI regulations if necessary.

Customs Compliance: Ensure compliance with customs regulations for the clearance of exported goods.

Goods and Services Tax (GST): Comply with GST regulations applicable to exports, including zero-rated supply provisions.

General Compliance Considerations

KYC Norms:

Both importers and exporters must ensure compliance with Know Your Customer (KYC) norms as required by financial institutions.

Foreign Direct Investment (FDI):

FDI regulations need to be followed based on sectoral caps and entry routes (automatic or approval).

Reporting of FDI to the Reserve Bank of India (RBI) must be done in Form FC-GPR (for equity instruments) or FC-TRS (for transfer of shares) within specified timeframes.

Overseas Direct Investment (ODI):

Investments made by Indian entities in foreign businesses require adherence to ODI guidelines.

Reporting of ODI through Form ODI and maintaining compliance with limits and sectoral requirements is important.

Liberalized Remittance Scheme (LRS):

Individuals sending money abroad under LRS (up to USD 250,000 per year) must ensure transactions are for permissible purposes like education, travel, and gifts.

Banks facilitating remittances need to monitor LRS usage for FEMA compliance.

Reporting and Documentation:

Every foreign exchange transaction must be reported to the RBI as per the regulatory framework, often through the Authorized Dealer Banks (ADs).

Non-compliance can result in penalties, fines, or legal action under FEMA.

?")

FEMA governs all foreign exchange transactions in India. It is essential for companies and individuals involved in foreign exchange to comply with FEMA regulations. Key compliances include:

FEMA governs all foreign exchange transactions in India. It is essential for companies and individuals involved in foreign exchange to comply with FEMA regulations. Key compliances include: